A System of Interconnected Modules

|

Our products are industry standard, which means that you can use them right out of the box, but the templates are completely customizable by you. Quality Control plans, mortgage policies and procedures and operations manuals are customizable in Microsoft Office formats. Implement best practices and create internal controls for your firm.

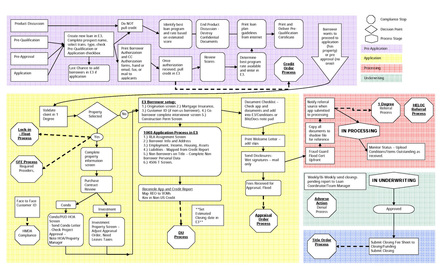

What are Modules? Because there are over 1800 individual processes and functions in the loan process, the logical way to organize the process is by function. We assign each procedure into a job function -origination, processing, underwriting, closing, post closing audit, compliance, operations servicing, secondary marketing and wholesale lending - and that function becomes a "module". If you only need one area, you purchase that module. If you are trying to run a company, you need the entire mortgage quality control plan package. What is a Template? When you think of a template, you may visualize a "fill in the blanks" kind of document. That is not what we mean. You can completely alter any of our products. A template is the way we control the formatting of a large document. The template makes sure all of the sections and headings appear in the table of contents. The table of contents acts like a navigation tool allowing you to jump directly to a specific part of a module. This also means that your procedures are easy to upload to and navigate in an intranet. Easy to Implement and Customize

Many customers use our products to update their current procedures. You can easily integrate procedures you have already written, and use our industry standard procedures to establish standards you haven't already written. |

Module Organization

Module customization, while it seems large a large task, can be delegated to the individual managers to edit, making it a team process.

Modules track to the individual functions in the loan process. This means you identify the ownership of a process with the job responsibility.

Each Module Contains:

|